|

Staff Paper Prepared for the President's Commission to Study Capital

Budgeting

CAPITAL ACQUISITION FUNDS

A. SUMMARY

This section is a summary discussion of capital acquisitions funds.

The subsequent section discusses an illustrative example of how such a

fund might work if applied to the Department of the Interior.

Issues

Capital acquisition funds (CAFs) might be useful in addressing the following

issues:

-

charging the use of capital uniformly and appropriately to programs so

that resources can be compared with the results achieved; and

-

ameliorating the "spikes" in budget authority and outlays that some agencies

incur for capital expenditures.

Discussion

For many programs, the cost of capital is not uniformly and appropriately

charged to the program, so that resources can be compared with the results

achieved. The acquisition cost of the capital may be paid by the program

up front in one year, so that the program has very large capital costs

in some years and little or no cost in other years. Alternatively, the

rental cost of using capital -- or the acquisition cost of the capital

-- may be paid by a central account, so that the program pays nothing.

The financial cost of holding capital (interest) is seldom charged to any

program.

Another problem is the scattering of capital asset acquisitions throughout

agency budget accounts. The result may be spikes in budget authority (BA)

and outlays for specific accounts that make it more difficult for the agency

to obtain funding within budget constraints, even if the agency's total

acquisition costs are at more regular levels. In some cases, the capital

costs are combined with operating costs. This makes the total cost of the

program less meaningful for analytical purposes, and spikes in capital

costs may squeeze out operating costs.

CAFs are a possible solution. There would be at least one such fund

in each department and major agency, more if necessary. They would only

finance the acquisition of capital assets and would get appropriations

of BA on a full funding basis. The BA would be in the form of authority

to borrow from Treasury. The CAFs would purchase the assets, using borrowed

funds, and rent the assets to one or more program accounts, charging a

rate sufficient to cover repayments of principal and interest on borrowing

from Treasury. The program account would outlay the rent out of funds appropriated

for operating expenses and the CAF would receive the rent as an offsetting

collection. (Thus, total budget authority and outlays -- and the surplus

or deficit -- would be unaffected.) Rental collections could only be used

by the CAF to repay funds borrowed from Treasury and to pay interest to

Treasury. They could not be used to finance new assets.

Pros:

-

Maintains principle of budgeting for the full cost of acquiring assets

up front: full funding of BA, and outlays measured up front by cash disbursements.

-

Allocates the cost of capital to program operating accounts in the form

of rent paid to the CAF for the annual use of the capital.

-

Ameliorates spikes by consolidating capital acquisitions within the agency

and thereby smoothing the BA and outlays for accounts within the agency.

-

Reduces crowding out in the program operating account by replacing upfront

capital costs with rent.

Cons:

-

Depends on shifting incrementally funded programs to full funding, which

Appropriations Committees rejected last year.

-

Requires a discretionary BA cap increase for the shift from incremental

funding over several years to BA at full funding levels in the first year.

Cap increases, even for conceptual reasons, sometimes meet political resistance.

(Using advance appropriations to accomplish full funding might obviate

the need for a cap adjustment, because the year to year changes in BA would

be smaller.)

-

The advocates of Government-wide consolidation and the congressional committees

that oversee GSA may object to the CAF concept, which limits aggregation

to the agency level.

-

Makes operating programs that do not currently include the cost of capital

appear more expensive, which may cause program proponents to resist.

-

Committees may attempt to "game" appropriations for rent (as they have

with GSA rent on occasions) by shorting the operating accounts. (OMB scored

no savings in the GSA case.)

-

There are some significant technical implementing issues -- how to treat

existing capital, how to handle differences between actual asset life and

the term of debt.

-

Complicates budget execution by adding borrowing and rental transactions.

CBO specifically endorsed this proposal in its testimony. Senator Enzi

and the Federal Executives Institute made roughly similar proposals.

Options

Current cost vs. historical cost.--The approach described above

uses historical cost as the basis for charging rent -- the rental payments

equal the amount needed to repay the debt incurred to finance the purchase

of the asset. There are practical advantages to this approach, not the

least of which is that it makes sense to people.

On the other hand, there is strong theoretical support for setting rent

at current market cost. It is the right measure for comparing the cost

of using resources for Federal vs. private purposes. It provides a level

playing field for selecting asset providers among the CAF, GSA (which charges

current market rent), and the private sector. A disadvantage is that it

creates a mismatch between the CAF's rental collections and its repayments

to Treasury. This could create balances and the temptation to use them

for other purposes.

Degree of consolidation.--CAFs would be useful for appropriately

budgeting capital costs even if there were one for every program. However,

if the capital costs of an agency were consolidated into fewer CAFs, they

would become more useful in ameliorating spikes in budget authority and

outlays. Some agencies could consolidate capital costs into one CAF. Those

with substantial capital for diverse missions reporting to different appropriations

committees may need more than one.

Experience with GSA's Federal Buildings Fund and the Information Technology

Fund shows that consolidation above the agency level can create management

and decisionmaking problems. For example, GSA's failure to anticipate the

full impact of Federal downsizing in FY 1996 and 1997 contributed to a

major shortfall in rent. Agency heads are better able and have more incentive

to determine their agencies' needs and priorities.

B. ILLUSTRATIVE EXAMPLE OF HOW A CAPITAL ACQUISITION

FUND WOULD

WORK FOR THE DEPARTMENT OF THE INTERIOR

| What is a capital acquisition? |

For this purpose, the term means the purchase or construction

of physical assets--land, buildings, land, and major equipment--directly

by the Federal government for its own use. It excludes grants to others

for acquiring physical assets, and it excludes Federal expenditures for

the conduct of R&D and education and training.

|

| How are capital acquisitions currently distributed in Interior? |

Capital acquisitions occur in eight bureaus and nineteen budget accounts.

During fiscal years 1997-99 (as shown in the FY 1999 Budget), budget authority

for capital acquisitions ranges from less than $1 million for some accounts

to more than $500 million for one account. Attachment

A shows capital expenditures (budget authority and outlays) by bureau

and account in each of these fiscal years.

|

| How would CAFs change this distribution? |

Capital acquisitions could be consolidated into one fund for all of

Interior. However, this would combine acquisitions funded by two subcommittees

of the Appropriations Committee in both the House and Senate: the Energy

and Water Development Subcommittee, which is responsible for Bureau of

Reclamation programs; and the Interior and Related Agencies Subcommittee,

which is responsible for all other Interior programs. Because crossing

subcommittee jurisdictions would create many problems, Interior would probably

need two funds. Also, this example is hypothetical; Interior officials

might identify other reasons for not combining all capital acquisitions

into only two funds.

The CAF for the Bureau of Reclamation would consolidate acquisitions

in five of the bureau's accounts. Budget authority would be $418 million

in FY 1997, $372 million in FY 1998, and $357 millions in FY 1999.

A CAF for the balance of Interior would consolidate acquisitions in

seven bureaus and fourteen accounts. Budget authority would be $776 million

in FY 1997, $1,191 million in FY 1998, and $658 millions in FY 1999.

|

| Would this redistribution change program management and operating

responsibilities? |

No. The CAFs would be accounting devices, not new organizational units.

The same officials would make decisions about capital acquisitions at whatever

level they do this now. The same staff would take the actions necessary

to acquire the assets, arrange for maintenance, etc.

|

| Would CAFs change Congressional responsibilities? |

No. Currently, the budget authority for most capital acquisitions is

provided in annual appropriations acts and amounts are specified by account.

In some cases, the budget authority for an account funds both capital acquisitions

and operations.

The subcommittees responsible for each CAF would provide the same total

amount of budget authority to the CAF for capital investment as they provide

now to separate accounts. They could continue to earmark amounts for specific

programs or acquisitions, either in the appropriations language or in report

language.

For a few capital acquisitions, the budget authority is permanently

appropriated in standing authorizing legislation. This would not change

under the CAF concept. Although the two CAFs would be aligned with the

two appropriations subcommittees (because they would be responsible for

most of the budget authority), the appropriations subcommittees would continue

to be responsible only for the budget authority subject to annual appropriations.

The appropriate authorizing committees would continue to be responsible

for the budget authority that is permanently appropriated.

|

| Would there be any change in appropriations for capital

acquisitions? |

Yes. Although the amounts of budget authority and outlays appropriated

for capital acquisitions would not change, the type of budget authority

would. Regular budget authority, which allows program managers to incur

obligations and make outlays with no additional steps, is provided for

most capital acquisitions now. The CAFs would receive budget authority

in the form of borrowing authority.

CAFs would incur obligations for capital acquisitions using borrowing

authority, just like they do with regular budget authority, but they would

have to borrow the cash necessary to make outlays. They would borrow from

the general fund of the Treasury in amounts sufficient to cover the cost

of an acquisition (or class of acquisitions) for lengths of maturity that

would equal the estimated economic life of the asset (or class of assets).

Treasury would determine the interest rate based on the average interest

rate on marketable Treasury securities of comparable maturity. The CAFs

would have to repay the principal with interest.

|

| How would the CAFs generate the income to repay the principal and

interest? |

The CAFs would use the borrowed funds to acquire capital assets and

rent them to program operating accounts in the bureaus. For example, the

CAF might finance the construction of a park facility and rent it to the

National Park Service. The rent for a period would equal the amount of

the principal payment and interest owed to Treasury in that period for

that asset. The principal would be amortized over the life of the loan

like a regular mortgage.

|

| Would the CAFs be set up as revolving funds--that is, allow

them to accumulate rents and use them to replace existing assets or acquire

new ones, instead of repaying Treasury? |

No. Rental collections could only be used by the CAF to repay funds

borrowed from Treasury and to pay interest to Treasury. They could not

be used to finance new assets. Revolving funds revolve because their collections

are permanently appropriated to finance the fund's outlays. In effect,

this is a decision in advance to fund replacement assets or new ones without

subjecting them to the rigors of the budget and appropriation process in

the budget year. Revolving fund acquisitions using accumulated collections

don't have to compete with discretionary funds for other resource demands.

This is appropriate for some public enterprise funds, which conduct a cycle

of business-type activities and where customer demand regulates their expenditures.

But, for taxpayer financed acquisitions, it is important to justify asset

acquisitions in light of current priorities.

|

| How would the operating account pay the rent? |

The operating account would budget for the rent, along with its other

operating expenses, and would use part of the budget authority it receives

each year to pay the rent to the CAF. This would be a new requirement for

many programs--those that now finance their capital acquisitions directly.

However, many programs already rent capital from a working capital fund,

GSA, or the public. The CAF approach would facilitate comparison of the

cost of programs fairly with each other and with performance goals and

measures.

|

| If both the CAFs and the operating accounts get budget

authority, wouldn't that be double counting? |

No. It is true that, on a gross basis, budget authority for acquisitions

would be appropriated twice--once as the budget authority for the CAF for

the acquisition itself and incrementally over time for the program operating

account as rent. However, in any fiscal year, the budget authority and

outlays for the rental payment in the operating account would be offset

by a collection of the same amount in the CAF. The two transactions would

net to zero in the totals for Interior, for scoring discretionary spending

under the Budget Enforcement Act (BEA), and in the totals for the budget

as a whole.

Though not a double-count, the finance charges (the CAF must pay interest

on borrowing from Treasury), which are not charged now on most capital

acquisitions, would increase Interior's total budget authority and outlays.

The interest would be treated as mandatory spending, under the BEA. However,

interest is not scored and would not require Interior or the appropriations

subcommittees to make tradeoffs. Requiring the CAF to pay finance charges

and including them in the rent paid by the operating account is a means

of imputing this element of the acquisition cost to the Government to the

agency accounts. In the budget totals, the interest payment would be offset

by a receipt in the general fund of the Treasury.

Attachment B shows what would

be scored under the BEA for Interior accounts before and after establishing

CAFs. |

|

| What's the advantage of all of this extra accounting? |

The main advantage is better allocation of the cost of using capital

assets to the programs. For example, for FY 1998, Congress appropriated

$1,246 million of budget authority to the National Park Service's operating

account. This amount did not include $198 million of budget authority for

capital acquisitions, which was appropriated to the construction account.

Under the CAF system of accounting, the parks program wouldn't have been

charged with the $198 million in capital acquisitions in FY 1998. Instead,

it would have been charged rent each year until the CAF's borrowing from

Treasury was repaid. The rent would be paid from the operating account

and, therefore, reflected in the cost of park operations.

This would be a better method of measuring the full cost of program

outputs and outcomes. It would encourage program managers to improve their

use of resources. Currently, there is little incentive for managers to

do anything about underutilized assets; the cost is sunk. If the program

had to pay rent, however, managers would be encouraged to increase the

utilization of an asset--occupy it with other activities, rent it to someone

else, or request the CAF to sell it.

|

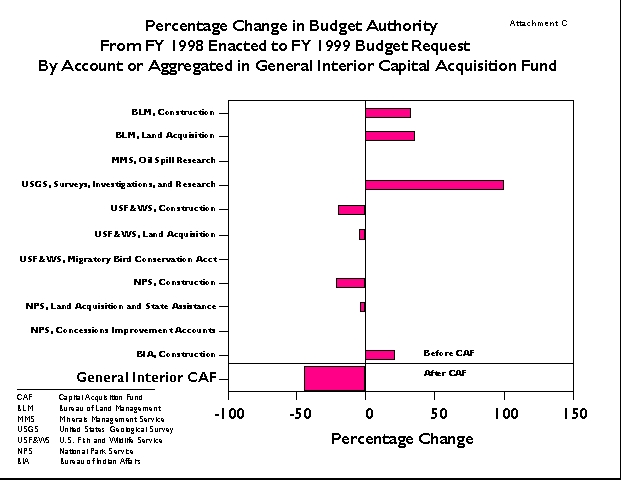

| Will CAFs help with "spikes" in budget authority and outlays? |

They will help. For example, some accounts in the Bureau of Land Management,

US Geological Survey, and Bureau of Indian Affairs showed significant budget

authority increases (ranging from 33 to 100 percent). The CAF containing

these accounts would have shown a decline in budget authority requested

of 45 percent. (See Attachment

C.)

|

| Aren't CAFs similar to GSA's Federal Building Fund? Would CAFs replace

GSA's fund? |

GSA's Federal Buildings Fund was created to acquire, manage, and share

use of common office space. It does not acquire other, specialized assets,

such as park facilities. The amounts for capital acquisition shown in this

Interior example are all for specialized assets that Interior is purchasing

currently, not for office space. CAFs would acquire the assets that agencies

now acquire, and GSA's responsibilities would not change. However, GSA

can and does delegate its authority to agencies to acquire their own office

space under some circumstances. In such cases, an agency would acquire

its office space through its CAF. Greater use of this delegation authority

would be appropriate if agencies could demonstrate that capital asset management

improved under their increased control.

|

Attachment A

Current

Distribution

of Capital Investments in the Department of the Interior

(in millions of dollars) |

|

|

|

Capital

Investments* |

|

Account

Total |

|

|

|

FY 1997 |

FY 1998 |

FY 1999 |

|

FY 1997 |

FY 1998 |

FY 1999 |

| BUREAU AND ACCOUNT |

BA |

OL |

BA |

OL |

BA |

OL |

|

BA |

OL |

BA |

OL |

BA |

OL |

| Bureau of Land

Management |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Construction................................... |

9 |

9 |

3 |

7 |

4 |

6 |

|

9 |

9 |

3 |

7 |

4 |

6 |

|

Land acquisition............................. |

10 |

9 |

11 |

18 |

15 |

18 |

|

10 |

9 |

11 |

18 |

15 |

18 |

| Minerals Management

Service |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Oil spill research............................. |

4 |

4 |

6 |

6 |

6 |

6 |

|

6 |

6 |

6 |

4 |

6 |

5 |

| Bureau of Reclamation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Water and related resources........ |

321 |

281 |

328 |

436 |

325 |

332 |

|

606 |

519 |

618 |

806 |

614 |

612 |

|

Lower Colorado River development |

57 |

55 |

8 |

(4) |

43 |

37 |

|

57 |

55 |

8 |

(4) |

43 |

38 |

|

Upper Colorado River.................... |

24 |

(25) |

21 |

72 |

3 |

9 |

|

24 |

(25) |

21 |

72 |

3 |

9 |

|

Working capital fund..................... |

0 |

(2) |

0 |

(26) |

(26) |

(1) |

|

0 |

(2) |

0 |

(26) |

(26) |

(1) |

|

Reclamation trust funds................ |

16 |

35 |

15 |

22 |

12 |

13 |

|

16 |

35 |

15 |

22 |

12 |

13 |

| United States Geological

Survey |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Surveys, investigations, and research |

5 |

5 |

1 |

1 |

2 |

2 |

|

138 |

139 |

145 |

143 |

158 |

158 |

| US Fish and Wildlife Service |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Construction................................... |

147 |

86 |

45 |

109 |

36 |

77 |

|

147 |

86 |

45 |

109 |

37 |

77 |

|

Land acquisition............................. |

54 |

41 |

63 |

57 |

60 |

60 |

|

54 |

41 |

63 |

57 |

60 |

60 |

|

Migratory bird conservation account |

42 |

41 |

40 |

40 |

40 |

40 |

|

42 |

41 |

40 |

40 |

40 |

40 |

| National Park Service |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Construction................................... |

322 |

225 |

198 |

200 |

156 |

199 |

|

340 |

243 |

215 |

217 |

175 |

218 |

|

Land acquisition and State assistance |

54 |

38 |

143 |

94 |

138 |

107 |

|

54 |

58 |

143 |

114 |

138 |

116 |

|

Concessions improvement accounts |

22 |

22 |

24 |

24 |

24 |

24 |

|

|

|

|

|

|

|

|

Park concessions franchise fee... |

0 |

0 |

0 |

0 |

25 |

9 |

|

0 |

0 |

0 |

0 |

25 |

9 |

|

Construction trust fund................ |

0 |

2 |

0 |

8 |

0 |

5 |

|

0 |

2 |

0 |

8 |

0 |

5 |

| Bureau of Indian Affairs |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Construction................................... |

107 |

113 |

125 |

128 |

152 |

118 |

|

107 |

113 |

125 |

128 |

152 |

118 |

| Departmental Management |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Priority Federal land acquisitions and

exchanges............................... |

0 |

0 |

532 |

228 |

0 |

114 |

|

0 |

0 |

532 |

228 |

0 |

114 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Capital Investment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Department.................................. |

1,194 |

939 |

1,563 |

1,420 |

1,015 |

1,175 |

|

|

|

|

|

|

|

|

|

Bureaus = 8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accounts = 19 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy&Water Dev. Cmte. (BuRec) |

418 |

344 |

372 |

500 |

357 |

390 |

|

|

|

|

|

|

|

|

|

Bureaus = 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accounts = 5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interior Cmte. (balance of Dept.) |

776 |

595 |

1,191 |

920 |

658 |

785 |

|

|

|

|

|

|

|

|

|

Bureaus = 7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accounts = 14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| * Direct expenditures (not grants) for physical

assets--in this case, buildings, land, and major equipment. |

Attachment B

BUDGET ENFORCEMENT ACT SCORING

OF CAPITAL

ACQUISITIONS

BEFORE AND AFTER ESTABLISHING CAFs

(dollars in thousands) |

|

|

|

|

|

|

Year 1

|

|

|

|

|

|

|

Before

CAFs |

After

CAFs |

|

|

|

|

|

|

Program

Operating

Account |

|

Program

Operating

Account |

Capital

Acquisition

Fund |

Total

BA |

| Discretionary budget

authority: |

|

|

|

|

|

|

|

Asset

acquisition............................................ |

10,000 |

|

0 |

10,000 |

10,000 |

|

Rent paid by operating account

1/............... |

0 |

|

644 |

0 |

644 |

|

Rent received by CAF

2/................................ |

0 |

|

0 |

-644 |

-644 |

|

|

Total discretionary budget

authority........................ |

10,000 |

|

644 |

9,356 |

10,000 |

| Mandatory budget authority: |

|

|

|

|

|

|

|

Authority to spend offsetting

collections... |

0 |

|

0 |

644 |

644 |

|

Less portion applied to debt principal

3/..... |

0 |

|

0 |

-148 |

-148 |

|

Interest

4/......................................................... |

0 |

|

0 |

496 |

496 |

|

|

Total mandatory budget

authority........................ |

0 |

|

0 |

496 |

496 |

|

|

Total budget authority...... |

10,000 |

|

644 |

9,852 |

10,496 |

|

|

|

|

|

|

|

|

|

| Notes: |

|

|

|

|

|

|

| -- The outlay rate for all expenditures

is assumed to be 100% and, since the amounts would be the same as for budget

authority, they are not shown. The outlay rate for rent and interest should

always be 100%. Outlays for asset acquistions might occur over more than

one year, especially if the asset is constructed, rather than purchased.

In any event, the outlays for acquisitions in any year after the asset

is put in place would be offset by $644 thousand in rent received. |

| -- This example assumes the asset is acquired

at the beginning of the fiscal year and rented for the entire year. |

| 1/ $644 thousand equals the mortgage payment

assuming a $10 million loan for 30 years at 5% with monthly repayments. |

| 2/ The offset for rent received is discretionary

because it cannot occur without the appropriation to the program account. |

| 3/ The budget does not record budget authority

or outlays for debt repayment (nor does it record receipts for borrowing).

When collections are used for debt repayment, they are unavailable for

new oblgations and, therefore, are not budget authority. |

| 4/ The interest payment will decline, and

the principal payment increase, in each subsequent year. The interest payment

will be credited to an intragovernmental receipt account in Treasury. It

is not scored for BEA purposes. |

Attachment C

President's Commission to Study

Capital Budgeting

President and First Lady | Vice President and Mrs. Gore

Record of Progress | The Briefing Room

Gateway to Government | Contacting the White House

White House for Kids | White House History

White House Tours | Help | Text Only Privacy Statement |